Until 30 June 2021, the UK government will continue contributing 80% of an employee’s wages for furloughed employees, capped at £2,500, but from 1 July this contribution will reduce on a sliding scale until the scheme ends at the end of September.

For July, employers will only be able to claim 70% of wages for furloughed staff, up to a maximum of £2,187.50

For August and September, employers will only be able to claim 60% of wages for furloughed staff, up to a maximum of £1,875

This means that employers who intend to continue to rely on the furlough scheme will need to make up the difference between what they can claim and what they are required to pay furloughed employees (80% of their wages, up to a cap of £2,500 per month for the time they spend on furlough) if they want to remain eligible for the CJRS grant.

With many employers still not able to fully reopen and many still struggling to generate revenue to cover existing operating cost, this additional uplift in costs may cause them to reconsider their position.

The long-awaited exit from lockdown has been delayed, with Prime Minister Boris Johnson warning a spike in cases of the Delta (Indian) variant could lead to a surge in hospitalisations.

COVID-19 Restrictions Continue to Impact UK Businesses

On Monday 14 June 2021, Prime Minister Boris Johnson announced that the full easing of all lockdown restrictions planned for 21 June 2021 in England has been potentially delayed by a period of 4 weeks, subject to a further review in 2 weeks’ time.

The devolved administrations of Scotland, Wales and Northern Ireland had previously announced an easing of restrictions which brought them closely in line with those restrictions set out at step 3 of the roadmap in England but considering the PM’s announcement on Monday it looks increasingly unlikely that any further easing of restrictions will be announced any time soon, or at least before the end of June.

A Disjointed Four Nations Approach to Lockdown Restrictions

Since the devolved administrations of Scotland, Wales and Northern Ireland decided to break lockstep with the UK government in favour of adopting their own approach to lockdown restrictions, many have been left confused and uncertain about what is or isn’t permissible.

In England, where a four-step roadmap out of lockdown is in place, more businesses were able to reopen when England moved to step 3, but the decision to delay the full easing of lockdown restrictions and remain at step 3 will create serious implications for employers who had hoped all COVID-19 restrictions would end on 21 June 2021 as originally planned.

In Scotland, where a five-tier protection system (0-4) is in place and which can be applied separately to each local authority area, more businesses were able to reopen from 5 June 2021 when many areas moved from level 3 to level 2 and from level 2 to level 1, subject to remaining social distancing restrictions, but soft play, nightclubs and adult entertainment venues must remain closed and many businesses in the tourism, hospitality and events sectors remain adversely affected.

In Wales, where a four-level alert system is in place (1-4), some restrictions were eased from 7 June 2021 when Wales moved from level 2 to level 1. Many more businesses were able to reopen, but skating rinks, nightclubs and adult entertainment venues must remain closed.

Covid-19 Restrictions in Wales

In Northern Ireland there has also been a slight easing of restrictions and many businesses have been able to reopen, but the overriding message is that working from home where possible should remain the default position and that employers should take every step possible to facilitate home working.

The Delay on Easing Lockdown Restrictions – Implications for Employers

The Prime Minister’s announcement was in response to a notable rise in the R number across all regions of the UK and continuing concerns over the impact of the Delta (Indian) COVID-19 variant.

For those businesses with employees currently working from home, the default position across all regions of the UK is that employees who can work from home should continue to do so.

There is no change to the guidance in respect of employees who cannot work from home – in these circumstances, employees continue to be permitted to work in their usual workplaces, and the working safely during coronavirus guidance continues to apply.

The delay in any further easing of lockdown restrictions is impacting all businesses, but those in the tourism, hospitality and events sectors appear to be affected most, not least due to continuing restrictions on how many people venues can safely accommodate with social distancing measures in place.

Practical Considerations for Employers

Many employers may also need to reassess their staffing requirements and quickly decide what this means for any recent job offers and current furlough arrangements and the cost implications of extending furlough beyond 1 July 2021 will need to be carefully considered.

Although the furlough scheme was previously extended until 30 September 2021, the level of grant available to employers will be reduced from 80% (up to a max. of £2,500):

From 1 July 2021 the grant available to employers reduces to 70% (up to a max. of £2,187.50).

From 1 August it will reduce again to 60% (up to a max. of £1,875).

Can an employer withdraw offers of employment or delay start dates for new recruits in light of the COVID-19 outbreak?

The first point to consider is whether a contract of employment has been entered into with the new recruits.

If the new recruits have accepted an offer of employment without conditions, and there is therefore a binding contract of employment, then notice would need to be served in order to terminate the contract before they commence employment. If there is a binding contract in force between the parties then any change in the start date will constitute a change in contractual terms. In this case, an employer would only be able to make a change to the start date either with the express consent of the new recruits or if it has an express contractual right to do so.

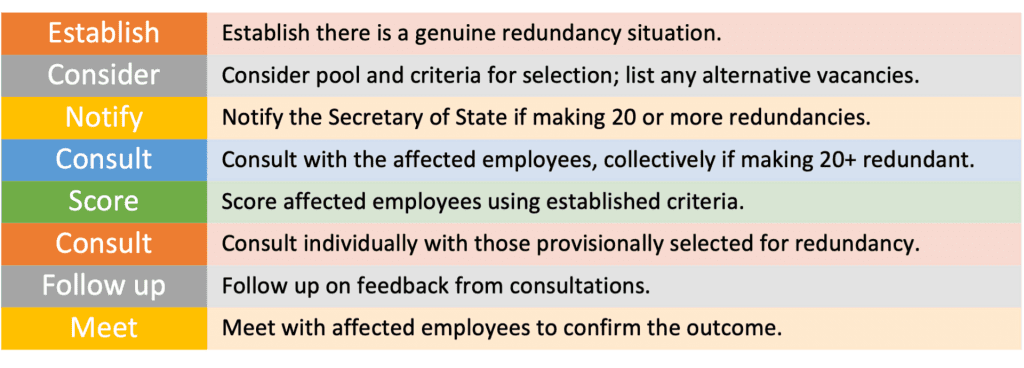

How should an employer go about making redundancies?

It may not always be possible for an employer to avoid making redundancies, even where alternatives are considered first. There are five principles for employers to follow when considering redundancies as a result of the COVID-19 pandemic:

Do it openly. The sooner people understand the situation, the better for everyone.

Do it thoroughly. People need information and guidance so ensure that you have trained staff representatives in how the redundancy process works.

Do it genuinely. Listen to people’s views before making a decision, be open to alternatives from individuals and unions and always feed back to them.

Do it fairly. Any redundancy procedure should be conducted fairly and without any form of discrimination.

Do it with dignity. Consider ahead how to handle the conversation and whether it will be face-to-face or remote. The way an employer makes redundancies says a lot about the organisation’s values.

On 26 May 2021, Kemi Badenoch MP, the Minister for Equalities, made a statement outlining that the gendered impact of the pandemic has not been clear cut. In summary, the Government confirmed that more men were made redundant during the pandemic than women.

Although women were furloughed at a disproportionate rate than men, she stated that the latest employment figures indicated that more men were made redundant than women. As a response, the government is working to address both men and women with its economic support measures.

Redundancy and the Impact of COVID-19

Despite the various resources intended to support businesses and protect jobs, an increasing number of employers are finding it difficult to retain current staff levels as COVID restrictions continue to impact.

With the CJRS ending in Septmber, many employers are now looking closely at redundancies.

Correctly identifying the circumstances that give rise to redundancies is the first step to ensuring any subsequent redundancy dismissals are fair.

A recent survey from Acas has found that over a third of employers (37%) are likely to make staff redundancies in the next 3 months. The poll found that:

6 out of 10 large businesses said they were likely to make redundancies in the next 3 months

for businesses that are likely to make redundancies, over a quarter (27%) said they plan to do this remotely over video chat or a phone call

1 in 4 (24%) bosses are unaware of the law around consulting staff before making redundancies – this increases to 1 in 3 (33%) where businesses have fewer than 50 workers

Circumstances That Can Give Rise to a Redundancy Situation

There are various circumstances that can give rise to a redundancy situation, including:

Diminished need for employees to do work of a particular kind.

Changes to terms and conditions where more than 20 employees are affected, and dismissal is a possibility.

Reduction in the numbers of employees doing a particular role.

Removal of a role or group of roles.

Closure of a department, site or entire business.

Many Employers often conflate the aforementioned circumstances with other reasons when considering redundancies, but they do so at their peril. For clarity, the following reasons do not give rise to a redundancy situation:

Issues of performance, conduct.

Where an external company could do the work better or more cheaply.

The same work could be done under different terms and conditions e.g. less qualified.

Where the employee is required to do additional work, but it remains “work of the same particular kind” and they refuse to do that.

Transfers of employment.

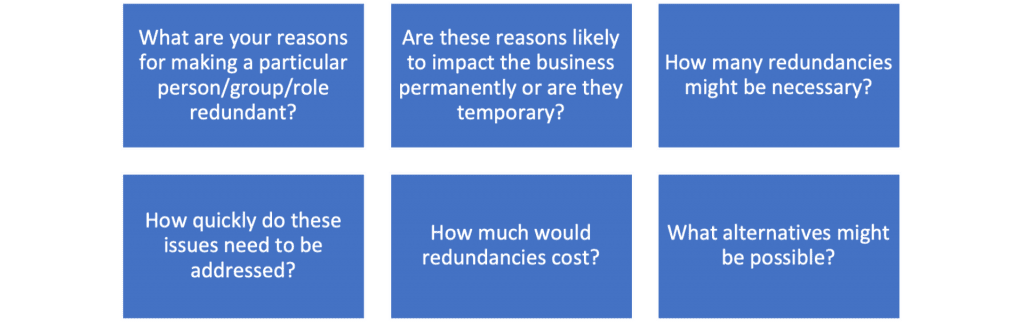

Before considering redundancies, it’s important that employers review the situation carefully before deciding to progress with redundancies. Key points employers should consider include:

Issues that need to be addressed in a redundancy situation:

Alternative to Redundancies

Employers have a legal obligation to consider how they might avoid compulsory redundancies. Some of the alternatives they should consider include:

Short time working and/or temporary layoffs – the new Job Support Scheme is intended to facilitate this.

Voluntary redundancy.

Temporary reduction in pay or hours.

Permanent reduction in pay or hours.

Redeploying to alternative roles and providing retraining (if reasonable).

Dismissing short service employees (where no risk and T&Cs allow).

Reducing/removing benefits.

Stopping/limiting overtime.

Other considerations include:

Is there a job that would be a suitable alternative within any associated business or alternative sites?

Does ‘Bumping’ apply? This is where an employee not previously at risk is put at risk to ‘save’ other employees.

Are any affected employees pregnant?

Are any affected employees on maternity leave?

Are any senior roles affected?

Employers will need to proceed with caution if any of the above scenarios apply.

If Making Less than 20 Redundancies

Under 2 years’ service:

If under 2 years’ service, and no risk of discrimination, a shorter process can be followed if the contract/handbook allow that.

No entitlement to redundancy pay, just notice pay.

Risk of discrimination or over 2 years’ service:

A minimum of three meetings (at risk, how can we avoid, if no ideas, dismissal).

If pools of candidates, objective criteria will need to be used relating to that particular role.

Scoring needs to be fairly done.

Right of appeal.

If Making 20 or More Redundancies

Where 20 or more employees to be made redundant at one establishment within 90 days:

Need to collectively consult with appropriate representatives.

Representatives are recognised trade union or employee representatives elected through a ballot.

Must provide prescribed information via HR1 to BEIS.

Must consult for at least 30 days before the first dismissal or for 100 days if more than 100 employees.

Right of appeal.

Protective award for a failure to consult = 90 days gross pay.

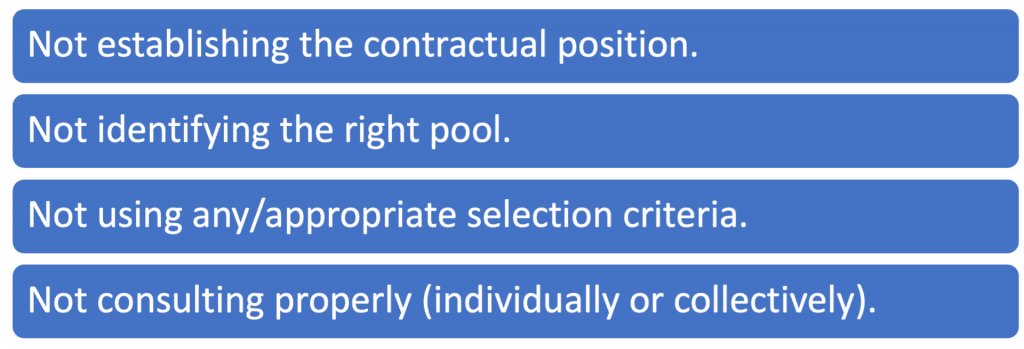

Where Most Employers Go Wrong With Redundancies

Employee Consultation

To avoid the risk of being deemed not to have consulted properly, employers need to consider the consultation process carefully and ensure:

Consultation is meaningful, with a view to getting agreement, not a means to an end.

It includes those off on long term sick leave, family friendly leave, fixed term (funding).

They involve a recognised union or collective consultation body (if authorised to consult on such matters), where required.

Letters are issued at each stage and 48 hours’ notice between meetings and the right to be accompanied is made clear.

Minutes are taken at each meeting.

The Implications of Getting Redundancies Wrong

Unfair dismissal claims

Not genuine redundancy (the real reason for dismissal).

The rescheduled UEFA Euro 2020 tournament kicks off in Rome on Friday 11 June 2021 and runs through to Sunday 11 July and many Employers may be faced with staff looking to watch their team during normal working hours.

With COVID-19 restrictions still in place across many parts of the UK and many employees still on furlough, this year’s tournament might be less impactful for UK employers, but many may still experience some difficulties as many excited football fans look to watch matches their teams are competing in.

With kick off times ranging from 2pm to 8pm, employees looking to watch matches could still phone in sick or worse, they might simply not turn up, and this could have serious implications for employers already struggling to get back to normal after enduring more than a year of COVID-19 restrictions.

To help Employers better understand the risks and equip them with tools to better manage the situation and create a positive outcome for both employer and employee, we’ve outlined below a few keys points Employers should consider.

Potential Issues Employers Might Face

Unauthorised absence

Staff being drunk / under the influence of alcohol at work

Inappropriate conduct by employees – discrimination, racism, bullying or harassment

Increases in holiday requests from both football and non-football fans alike

Ways Employers Could Avoid Issues

1. Ensure You Have Clear Policies in place including:

Sickness & Absence Policy

Code of Conduct

Discipline & Grievance Policy

Bullying & Harassment Policy

Drugs & Alcohol Policy

Equality & Diversity Policy

2. Manage absenteeism in advance.

Make it clear to employees that absences without authorisation will not be paid and may lead to action under the Disciplinary Policy.

Utilise Return to Work Interviews to identify and address fake sickness absence or absent resulting from post-match hangovers

3. Reconsider Your Holiday Arrangements

Relax caps on the number of employees that are allowed to be on holiday at one time

Where staff have indicated they want to see certain matches, encourage them to take the time off as annual leave.

Remember non-football fans may make holidays requests during the same period and so you will need to ensure you treat all holiday requests fairly and equally. Granting a holiday request by a male employee but refusing a holiday request from a female employee could trigger a claim of sex discrimination!

4. Some Other Things to Consider

Screening matches in a meeting room or communal area.

Relaxing your Internet Policy and allow employees to stream matches on their PCs.

You will need to ensure you have the appropriate licenses in place which allow screening or streaming of live TV within the workplace.

From 1st April 2021, national minimum wage rates increased but April sees a number of further changes to Employment Laws from 4 April 2021.

On 1 April 2021, we highlighted the changes to the National Minimum Wage Rates last week, but there are a number of further changes which come into effect from 4 April 2021 including, changes to statutory sick pay, statutory family leave pay, Employment Tribunal compensation awards and rates and IR35 legislation.

Statutory Family Leave

From 4 April 2021, the weekly rates of statutory family leave (maternity/paternity leave, etc.) increased by 77p per week, from £151.20 per week to £151.97 per week.

Statutory Sick Pay

From 6 April 2021, the weekly rates for Statutory Sick Pay increase from £95.85 per week to £96.35 per week. The lower earnings limit in relation to eligibility to statutory payments is to stay the same at £120 per week.

ET Compensation Awards and Rates

From 6 April 2021, employment tribunal compensation rates are to increase. The maximum week’s pay for redundancy pay purposes will increase from £538 to £544. This is important for the purposes of tribunal claims because it means that the maximum statutory redundancy pay, as well as unfair dismissal basic award pay, will both now be £16,320. The unfair dismissal compensatory award, which is set to compensate the claimant for past and future lost attributed to the dismissal, is a maximum of 52 weeks’ pay, subject to a new maximum of £89,493.

The maximum amount of additional award for unfair dismissal, set to compensate claimants when employers fail to adhere to a tribunal instruction to re-engage them, taking into account average weekly earnings, will rise to £28,288.

IR35 Legislation

The IR35 legislation, which aims to ensure that contractors are paying the appropriate amount of tax, is also changing for some private sector businesses. Currently, most contractors are required to determine their own status as employee or contractor; however, from 6 April 2021, this liability will pass to medium and large-sector clients. Smaller clients will be exempt from this obligation, and the contractor remains liable for determining their own tax status.

From 1st April 2021, national minimum wage rates increase and the National Living Wage age threshold reduces.

The new national minimum wage hourly rates, which come into effect from 1 April 2021 are as follows:

Workers aged 23 and over (National Living Wage) – £8.91

Workers aged 21-22 – £8.36

Development rates for workers aged 18–20 – £6.56

Young workers rate for workers aged 16–17 – £4.62

Apprentices under 19, or over 19 and in first year of the apprenticeship – £4.30.

And don’t forget…..the National Living Wage (NLW) threshold is also lowering to include all those aged 23 and over. Currently, the NLW is payable only to people who were aged 25 and over.

After losing it’s lengthy Supreme Court battle just less than one month ago, Uber have announced it will give its 70,000 UK drivers a guaranteed minimum wage, holiday pay and pensions.

Last month we confirmed Uber’s lengthy legal battle to overturn the 2016 Employment Tribunal (ET) decision had finally came to an end when the Supreme Court unanimously ruled against them and concluded drivers should be classed as workers, not independent third-party contractors – https://employmentlawservices.com/uber-loses-landmark-supreme-court-battle-over-workers-rights/

In the weeks following the Supreme Court’s ruling, Uber have carefully considered their position and announced yesterday that it will give its 70,000 UK drivers guaranteed minimum wage, holiday pay and pensions. The taxi company confirmed that all drivers can expect to earn at least the National Living Wage for over-25s, irrespective of age, after accepting a trip request and after expenses, that they will be entitled to paid holiday based on 12.07% of their earnings, which will be paid on a fortnightly basis, that they will also be enrolled into a pension plan automatically, with contributions from Uber, that they will continue to receive free insurance in case of sickness or injury as well as parental payments, which have been in place for all drivers since 2018 and retain the freedom to choose if, when and where they drive.

It will be interesting to see if Uber will extend this decision to its food delivery business, Uber Eats, which remains unaffected by this decision.

The Supreme Court ruling in this case was always going to have far-reaching implications for millions of people working in the gig economy and the companies that employee them, but only time will tell whether other employers operating in the gig economy will follow Uber’s lead.

In his Spring 2021 Budget, the Chancellor announced that the Coronavirus Job Retention Scheme (CJRS) will be extended for a further five months from May until the end of September 2021.

Chancellor Rishi Sunak said the scheme – which pays 80% of employees’ wages for the hours they cannot work in the pandemic – would help millions through “the challenging months ahead”.

Key Highlights Announced by the Chancellor

Employees will continue to receive 80% of their current salary for hours not worked.

There will be no employer contributions beyond National Insurance contributions (NICs) and pensions required in April, May and June.

From July, the government will introduce an employer contribution towards the cost of unworked hours. This will be 10% in July and 20% in August and September.

For periods ending on or before 30 April 2021, employers can claim for employees if they were employed on or before 30 October 2020, as long as they have made a PAYE Real Time Information (RTI) submission to HMRC between 20 March 2020 and 30 October 2020. This may differ if employees were made redundant, or they stopped working for the employer on or after 23 September 2020 and were then re-employed by the employer.

For periods on or after 1 May 2021, employers can claim for employees if they were employed on 2 March 2021, as long as they have made a PAYE Real Time Information (RTI) submission to HMRC between 20 March 2020 and 2 March 2021.

Do employers need to enter into fresh furlough agreements with employees from 1 May 2021?

As a result of the CJRS being extended to 30 September 2021, there will be several potential scenarios for Employers to consider, including:

An employee who was already furloughed before 30 April 2021 under an agreement without an end date.

An employee who was not already furloughed under the CJRS.

An employee who was already furloughed before 30 April 2021 under an agreement without an end date

Where an employee was furloughed under a written furlough agreement entered into before 31 October 2020 which remains in force, it may be possible for the previous furlough arrangement to simply continue after that date.

The requirements of a valid furlough agreement under the fifth Treasury direction are the same as previously under the third Treasury direction (see paragraph 7.1, fifth Treasury direction) and at this time there is no requirement for the agreement to be entered into on or after 1 November 2020. The only requirement is that it is entered into before the period to which the claim relates (paragraph 7(c)(i)). Assuming the eligible employer and qualifying employee requirements continue to be met (which also remain substantially the same under the fifth Treasury direction, see paragraphs 4 and 6), it may be possible for furlough to continue under a previous furlough agreement.

However, it is likely that some amendment will be required to most furlough agreements in order for the arrangement to continue after 30 April 2021.

An employee who was not already furloughed under the CJRS

As the employee was not furloughed previously, the employer should enter into a detailed furlough agreement with the employee and the employee should be asked to sign and return the agreement to confirm their agreement to be furloughed in accordance with the terms of the CJRS. This could be done electronically.

The agreement should be made before the CJRS period to which it relates starts.

What About Self-Employed Workers?

The Chancellor announced that the Self-Employment Income Support Scheme (SEISS) is also being extended with a fourth grant covering the period February to April 2021 and a fifth and final grant covering May to September 2021.

There will be temporary continuation of tax exemptions for COVID-19 tests and home office expenses, and of the Statutory Sick Pay (SSP) Rebate Scheme while sickness levels remain high.

In a recent survey 23% of employers said they plan to require staff to be vaccinated, but can employers impose a mandatory vaccination requirement on their employees?

The Law on Mandatory Vaccinations

Although current legislation (the Public Health (Control of Disease) Act 1984 and the Coronavirus Act 2020), already gives the UK Government and devolved Administrations the power to make regulations to prevent, protect against, control or provide a public health response to the incidence or spread of infection or contamination, there is no legislation to mandate COVID-19 vaccinations and the Health Secretary, Matt Hancock, has stated that the government is not considering introducing legislation to make vaccinations compulsory.

So, Can Employers Require Employees to be Vaccinated?

In the absence of it becoming a legal requirement an employer cannot force an employee to be vaccinated without their consent. Vaccination without consent could amount to the criminal offences of assault.

An employer considering imposing a mandatory vaccination requirement, or treating employees or job applicants differently because of their vaccination status, should consider the following:

Vaccination is not suitable for everyone.

Requiring an employee to be vaccinated without their consent as a condition to providing work could amount to a repudiatory breach of contract, entitling them to claim constructive dismissal.

There are potential reasons where a mandatory requirement to be vaccinated could be indirectly discriminatory against certain protected characteristics and a breach of Article 8 of the European Convention on Human Rights.

Currently, private vaccination is not available. All individuals must wait their turn, in order of priority, to be offered vaccination. Allowing only vaccinated employees to return to the workplace could potentially lead to indirect or direct age discrimination claims by younger employees, although both direct and indirect age discrimination can be justified.

A vaccination requirement may be difficult to justify on health and safety grounds. Although vaccination reduces the chance of the vaccinated individual becoming ill, the extent to which vaccination reduces transmission is still under review. Although the Guide for healthcare workers states that it is likely that vaccinated healthcare workers will be less likely to pass on infection as the viral shedding period will be shortened. Further, it is not yet known how long protection from vaccination will last. The current advice is clear that vaccination is not a substitute for workplace COVID-secure measures which must continue to be complied with.

Imposing a mandatory vacation requirement could result in negative publicity for the employer which could have a detrimental impact on business profitability, employee retention and recruitment.

There is a very small risk that vaccination could have long-term adverse side effects for some individuals. A cautious employer may also be concerned about the risk of an employee having an adverse reaction to the vaccine. An employee who was compelled to obtain the vaccine and who suffers an adverse reaction, may attempt to bring personal injury proceedings against the employer. For information on potential waivers in this respect.

Consultation with workplace and health and safety representatives, and with trade unions, is likely to be required.

There are data protection implications of requiring employees to provide information on their vaccination status, verifying its accuracy, and retaining that data.

In theory, an employer could decide to prevent unvaccinated employees from entering the workplace or restrict their duties. This could in turn adversely impact an unvaccinated employee’s pay. Preventing an employee from coming to work risks leaving the employer in breach of contract and could give rise to claims of constructive dismissal if the employee resigns in response or is dismissed.

The Acas guidance advises that employers should support staff in getting the vaccine but cannot force them to be vaccinated. However, it acknowledges that it may be necessary to make vaccination mandatory where it is necessary for someone to do their job, for example where they travel overseas and need to be vaccinated.

Alternatives to Mandatory Vaccination

Employers considering alternatives to mandatory vaccination may prefer to encourage voluntary vaccination within their workforces as an alternative to mandatory vaccinations. Taking advantage of the information currently available on the potential advantages and disadvantages of vaccination, Employers could communicate this to staff to assist them in making an informed decision. Doing so would be in accordance with an employers’ duty of care and obligation to take reasonable steps to provide a safe workplace and safe system of work.

Additional alternative measures employers should consider include:

regular testing for frontline staff (only available in England – https://www.gov.uk/get-workplace-coronavirus-tests);

regular health and safety reviews to ensure that the employer is up to date with, and properly implementing, the COVID-secure guidelines for its particular industry.

allowing employees to work from home, where possible; or

temporarily changing employee roles or responsibilities to minimise the workplace risk as far as possible.

Uber has lost its battle in the Supreme Court over drivers’ rights – a decision that could have far-reaching implications for millions of people working in the gig economy.

Back in November 2017 we reported that the Employment Appeal Tribunal (EAT) rejected taxi firm Uber’s attempt to overturn the 2016 Employment Tribunal (ET) ruling that two drivers who were employed as gig-economy contractors by Uber should have been classed as ‘workers’ under the Employment Rights Act 1996, not as self-employed. At the time, Uber made it clear that they intended to appeal and after failing to overturn the EAT’s decision at the Court of Appeal, the case was heard by the Supreme Court on 21 and 22 July 2020.

Supreme Court Judgement in the Uber Case

On 19 February 2021, Uber’s lengthy legal battle to overturn the 2016 Employment Tribunal (ET) decision finally came to an end when the Supreme Court issued its Judgement. The UK’s highest court unanimously ruled against Uber and concluded drivers should be classed as workers, not independent third-party contractors, which means they are entitled to basic employment protections, including minimum wage and holiday pay.

In the 42-page Judgement, the court rejected Uber’s argument that it merely acted akin to a booking agent for drivers, noting that the company would have no means of performing its contractual obligations to passengers (nor complying with its regulatory obligations as a licensed private hire vehicle operator) — “without either employees or subcontractors to perform driving services for it”.

Implications the Supreme Court Judgement Will Have for Other Employers

The Supreme Court’s judgement is likely to cause massive implications as other companies with large self-employed workforces may now face very similar action, particularly companies like Deliveroo and UberEats who engage drivers to deliver food. It is expected that organisations who have adopted a similar model to Uber will now discover that they owe a substantial amount more to their workers, such as paid annual leave, national minimum wage and sick pay.

Understanding Employment Status

An increase of atypical contracts has effectively blurred the lines between self-employed and employed status and so employers should be very careful when entering into any sort of working relationships. A basic explanation of each status/category is as follows:

Employee: Under section 230(1) of the Employment Rights Act 1996 (ERA 1996) an employee is defined as “an individual who has entered into or works under (or, where the employment has ceased, worked under) a contract of employment”. Under section 230(2) of ERA 1996, a contract of employment means “a contract of service or apprenticeship, whether express or implied, and (if it is express) whether oral or in writing”.

Worker: A worker is defined under section 230(3) of ERA 1996 as an individual who has entered into or works under (or, where the employment has ceased, worked under) a contract of employment; or any other contract, whether express or implied and (if it is express) whether oral or in writing, whereby the individual undertakes to do or perform personally any work or services for another party to the contract whose status is not by virtue of the contract that of a client or customer of any profession or business undertaking carried on by the individual.

Self-Employed: A person is self-employed if they run their business for themselves and take responsibility for its success or failure and they aren’t paid through PAYE.

Significance of Making the Correct Distinction

The distinction between the three categories is significant for a number of different reasons, including the following:

1) Employers and employees have obligations that are implied into the contract between them (for example, the mutual duty of trust and confidence). Some core legal protections only apply to employees, most particularly the rights on termination of employment granted under ERA 1996 (the right not to be unfairly dismissed and the right to receive a statutory redundancy payment). As mentioned above (see Worker status), workers enjoy limited protection under employment law.

2) Only employees are covered by the Acas Code of Practice on Disciplinary and Grievance Procedures

3) Only employees will be automatically transferred to any purchaser of their employer’s business under the Transfer of Undertakings (Protection of Employment) Regulations 2006 (SI 2006/246).

4) The tax and social security treatment of a person providing services depends on their status.

5) An employer is vicariously liable for acts done by an employee in the course of their employment. This vicarious liability is unlikely to extend to independent contractors or self-employed individuals.

6) An employer is required to take out employer’s liability insurance to cover the risk of employees injuring themselves at work. Self-employed individuals or independent contractors may not, in every case, be covered by this insurance and may want to consider entering into appropriate insurance for their own benefit.

7) Employers owe employees statutory duties relating to health and safety. Independent contractors may not be covered under these duties although they will be covered under the employer’s common law duty of care in respect of occupier’s liability.

Employees, workers and self-employed workers enjoy a variety of different legal entitlements, and since many of these rights form the basis of the employment status, the consequences of getting an individual’s employment status wrong should not be underestimated.

Advice on Settlement Agreements Employees

Advice on Settlement Agreements Employees Advice on Settlement Agreements Employers

Advice on Settlement Agreements Employers